Agricultural News

Wheat Marketing Year Proved Exceptional in Review

Fri, 10 Jun 2011 11:47:31 CDT

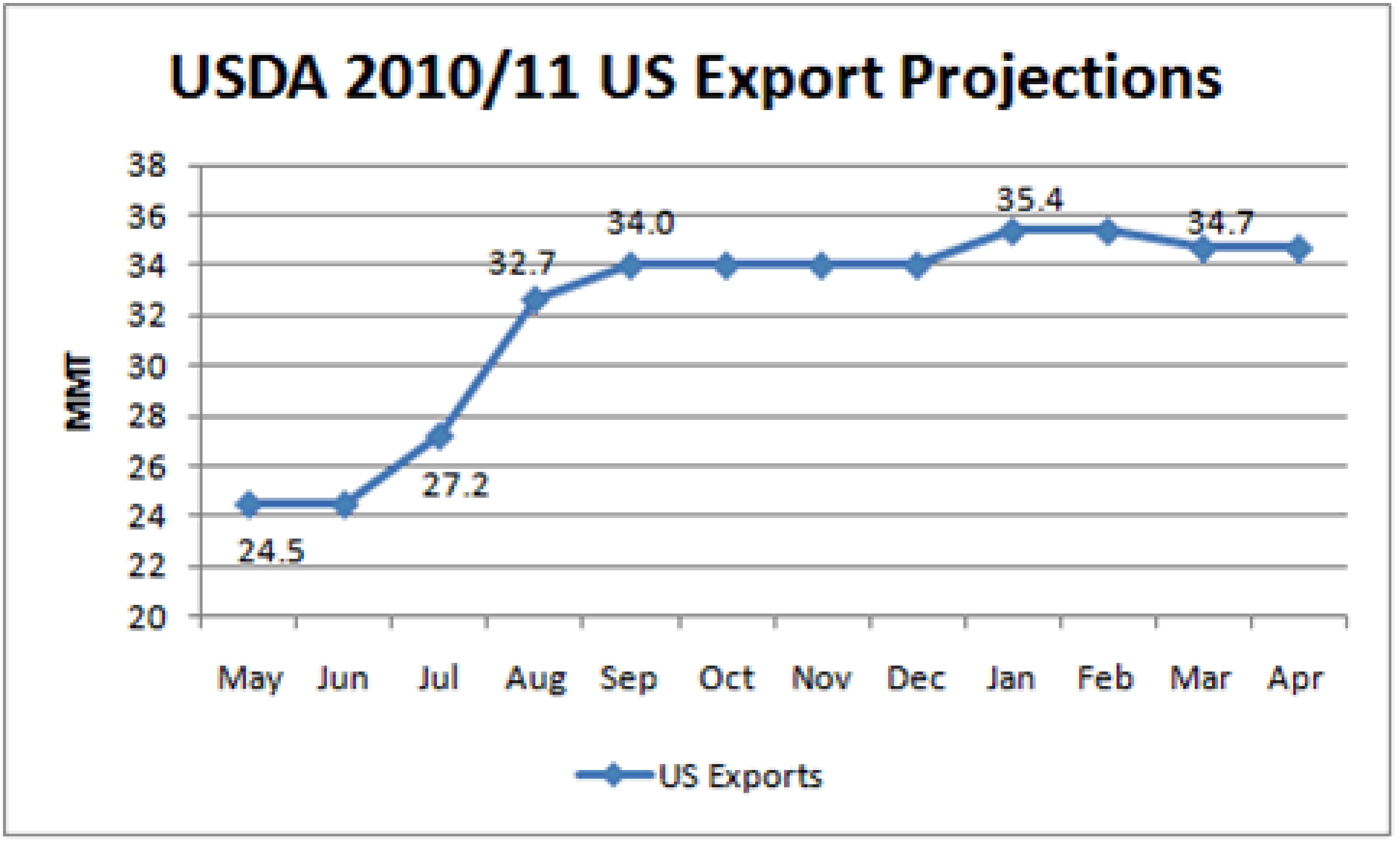

Just one year ago, MY 2009/10 ended sluggishly for U.S. wheat demand. Commercial sales stood at 22.7 million metric tons (MMT), the lowest total in 29 years. With what appeared to be abundant supplies of lower priced Black Sea wheat, most analysts and the U.S. Department of Agriculture (USDA) had similar expectations for 2010/11. USDA's initial 2010/11 estimates showed only a slight increase in U.S. wheat exports to 24.5 MMT.

Just one year ago, MY 2009/10 ended sluggishly for U.S. wheat demand. Commercial sales stood at 22.7 million metric tons (MMT), the lowest total in 29 years. With what appeared to be abundant supplies of lower priced Black Sea wheat, most analysts and the U.S. Department of Agriculture (USDA) had similar expectations for 2010/11. USDA's initial 2010/11 estimates showed only a slight increase in U.S. wheat exports to 24.5 MMT.

News about dry conditions in Russia, Ukraine and Kazakhstan first appeared in June 2010 and grew more ominous through July. Then, just as importers were absorbing the potential impact of the deepening drought, Russia's government shocked the markets by halting wheat and feed grain exports. Ukraine and Kazakhstan quickly implemented grain export quotas.

Because the importers that were counting on Black Sea supplies are kept informed through the 15 overseas offices for U.S. Wheat Associates (USW), they knew they could rely on the U.S. wheat supply to meet their needs immediately and throughout the marketing year. In just one month, USDA's U.S. export projection jumped more than 40 percent to 32.7 MMT.

That number continued to grow (see chart) as additional weather problems affected the Canadian, German and Australian wheat crops. Ultimately, U.S. commercial export sales reached 35.3 MMT in 2010/11, a 56 percent increase from 2009/10 and the highest level since 1992/93.

The largest growth in 2010/11 export sales came from the Middle East/East Africa region. U.S. wheat imports for Middle East/East Africa reached 8.7 MMT this year, compared to 1.5 MMT last year. The top buyer of U.S. wheat in 2010/11 was Egypt, with purchases reaching 4 MMT in 2010/11. Iraq also relied heavily on U.S. supplies in 2010/11, importing 1.3 MMT compared to 305,000 metric tons (MT) in 2009/10.

With the Australian wheat supply down due to quality and logistical issues, the South Asian region had the second largest increase in U.S. wheat imports in 2010/11. South Asia purchased 3.9 MMT, up 38 percent from 2009/10. Imports by Indonesia, where Australia traditionally has a 55 percent market share, reached 840,000 MT, a 59 percent boost from 2009/10. Purchases by the Philippines, the largest U.S. wheat buyer in the region, climbed from 1.6 MMT to 1.9 MMT, the highest level in the past 10 years.

The European Union (EU) more than doubled its U.S. wheat purchases in 2010/11 following production and quality setbacks from the second largest producer in the region, Germany. The EU bought 1.8 MMT of U.S. wheat in 2010/11, compared to 820,000 MT the year prior. This included imports of 790,000 MT of hard red spring (HRS), which accounted for 55 percent of the EU's total increase.

In fact, all regions except North Africa increased U.S. wheat imports in 2010/11. South America increased imports by 38 percent to 2.7 MMT, with Peru nearly doubling its U.S. imports to 1 MMT. Sub-Saharan Africa increased imports by 24 percent to 4.6 MMT. Nigeria, last year's top U.S. buyer, was the second largest importer in 2010/11 with imports of 3.9 MMT. Imports by North Asia and the Mexico/Central America/Caribbean region both reached 6.2 MMT, increases of 15 percent and 16 percent respectively. While imports by North Africa fell by eight percent, increases were recorded for both Tunisia and Libya.

Looking to 2011/12, USDA projects continued strong demand for U.S. wheat. USDA currently projects 2011/12 exports at 28.6 MMT, just above the 10-year average of 28.3 MMT. However, as the Black Sea drought and the supply shock of 2010/11 prove, the final results depend on weather, government actions and many other factors. One thing the world's wheat buyers do know: U.S. wheat remains "the world's most reliable choice."

WebReadyTM Powered by WireReady® NSI

Top Agricultural News

More Headlines...

{kind=link}